What is lease accounting?

Lease accounting is the process by which companies and organizations record the financial impact of agreements to rent or finance the rights to use specific assets, more simply known as leasing. Recent accounting pronouncements have changed the way lessees and lessors are required to account for and report their leases.

The terms “lessor” and “lessee” are used to identify the different parties involved in a lease agreement. This distinction is important, because lease accounting as a lessor is significantly different from lease accounting as a lessee. When the various accounting boards for the domestic, international, and government entities issued new lease accounting standards, the underlying definitions of lessor and lessee did not change. However, some of the accounting treatment for lessors and lessees under the new lease standards did change.

Lessor vs. lessee

Lessor definition

A lessor is defined as an entity (i.e. a person, a company, or an organization) that provides the right to use an asset for a period of time in exchange for consideration. One of the more common scenarios of a lease agreement is an entity renting their owned property to another entity for a monthly cash payment. For example, if an organization owns a building and leases the right to use the building or space within the building, the owner of the building is the lessor.

Lessee definition

A lessee is defined as the entity paying for the use of specific property from a lessor. For example, if a person leases a vehicle from a car dealership, the person using the car is the lessee. Conceptually, the lessee is paying the lessor for the “right to use” this asset. This is why the lessee, in accordance with the new lease standards, is required to recognize an intangible “right-of-use asset” (ROU asset) or a “lease asset” when accounting for the lease. It is important to note this asset is classified as an intangible asset on the lessee’s books, rather than a fixed asset.

Lessee vs. lessor accounting

The FASB, GASB, and IASB have released new lease accounting standards over the last several years. The primary change to lease accounting is that organizations must now recognize lease assets and lease liabilities on the balance sheet for most of their lease arrangements. For GASB specifically, lessors will mirror the accounting on the lessee side, recognizing a lease receivable and deferred inflow of resources. The governing boards created new standards for lease accounting based on feedback from investors and users of financial statements requesting more visibility regarding future lease obligations and lease receivables.

Under the new lease accounting standards, lessees are required to calculate the present value of future lease payments to establish a lease liability and the related ROU asset. The lessor accounting differs depending on the standard. Below are summaries of lessee and lessor accounting under ASC 842, IFRS 16, and GASB 87.

ASC 842

Under ASC 842, the new lease accounting standard for US companies following US GAAP, lessees are required to recognize lease assets and lease liabilities on their balance sheets for both operating and finance (previously capital) leases. The lessee is required to perform a present value calculation of future expected lease payments to establish the lease liability and the related ROU asset. Accounting for leases classified as operating leases is affected the most, as leases classified as capital leases were already recognized on the balance sheet under ASC 840.

The accounting for the lessor is largely unchanged from ASC 840 to ASC 842. Lessors continue to recognize lease income for their leases, and balance sheet recognition requirements stay predominantly the same. The lease agreement’s underlying asset will continue to be classified as the lessor’s fixed asset.

Under ASC 842, there are 3 types of lessor leases:

- Direct Financing – lessors are required to establish a lease receivable and interest income

- Sales Type – lessors are required to establish a lease receivable and interest income. The difference between direct financing and sales type leases is revenue (With a sales type, the lessee has control of the underlying asset and the lessor recognizes sales revenue and profit at lease commencement)

- Operating – lessors recognize income on a straight line basis

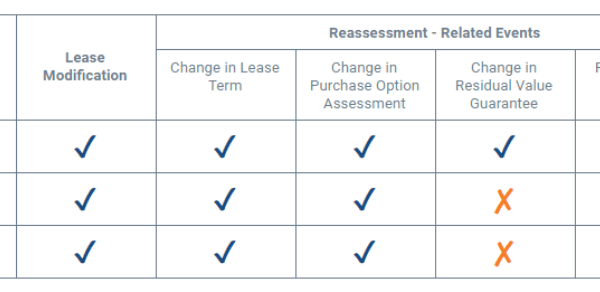

Lessees and lessors have the option to elect a package of practical expedients, in which the lessor is not required to reassess lease classification. Therefore, we expect many lessors to elect this expedient and retain previously established lease classifications when transitioning from ASC 840 to ASC 842.