|

| Image Attribution: www.dreamstime.com |

Lease rates for industrial properties in Southern California continue to rise! To place this in some context, if your direction – as a business owner – was to rent a location in 2011 and your operation consumed 100,000 square feet – you could expect to pay around $45,000 per month in rent. Of course, charges for things like property taxes, insurance and maintenance would have been in addition to the $45K. But, the additional charges would have added around $12,500 per month – bringing the total to $57,500 – $.575 per square foot. Flash forward to our pandemic fueled shortage of space these days and a comparable building leases for $135,000 per month! For those scoring at home – that’s a 134% increase in ten years. Or, a 13.4% annual increase. Simply nuts! Am I saying if you rented an address in 2011 and signed a ten year lease – when your lease expires this year – you can expect your rent to more than double? Yes! You got it. Wow! How are businesses able to afford such a whopping spike? Better still, are there strategies you can employ to stem the bumps? The answers are – I don’t know and yes. Indulge me as I outline a few ways to lessen the blows of gigantic rent inflation.

Know your owner. The gentleman to whom you send your rent each month, falls into a category of investors. Your tenancy is singular or multiple. Unfortunately, if you’re one of many and his buildings are full – your leverage is limited. You see, he may opt to push rents even if a move-out ensues. He’ll simply replace you. Conversely, if your rent is the biggest part of his retirement income – a bit more realism happens. If you relocate – and his music stops – so does his lifestyle. He’ll be more flexible with you to keep you in residence and avoid a costly vacancy.

Know your value. As a tenant, your worth is two-fold. First, the capitalized income you pay each year determines the dollar amount of the investment. Simply, $100,000 in annual rent – at today’s cap rates of 4.75% suggests $2,105,263 ($100,000/4.75%) – if a sale or refinance was considered. Why is this important? A bank would lend a percent of this amount if your owner needed cash. Plus, the market would gladly pay him this figure if a decision was made to cash-in or redeploy the money into another income property. Second, your tenancy is costly to replace. By this I mean – free rent, downtime, refurbishment, and professional fees – are forked over to secure a paying customer. So, let’s say the title holder of your location believes he can get $100,000 a year if you bolt. You currently pay him $80,000. If he’s correct in his assumption – he can achieve approximately $538,406if he’s finds a five year tenant ($100,000 with a 3% annual rent escalator). However, if he lays fallow for two months, incentivizes the new group with one month of free time, paints and carpets the offices, and pays a commercial real estate professional 6% – count on an up front expenditure of $72,303 – ($16,666 for downtime, $8333 in free rent, $15,000 for fix up, and $32,304 in fees). If we subtract $72,303 from our expected new income stream of $538,406 our net take is $466,103 – $93,220 per year. You’re willing to pay him $90,000. So, he could be slightly better off replacing you. But, if any of his assumptions are wrong – he sits four months vs two as an example, he is better off renewing you at $90,000 per year. Plus, presumably you’ve paid on time, taken care of the premises and sent him a Christmas card. Those intangibles have credibility. He may have to chase the new guy to get his rent.

Know your alternatives. Don’t forget. You could buy a building, consider a cheaper area or opt for a shorter lease term.

More on these later.

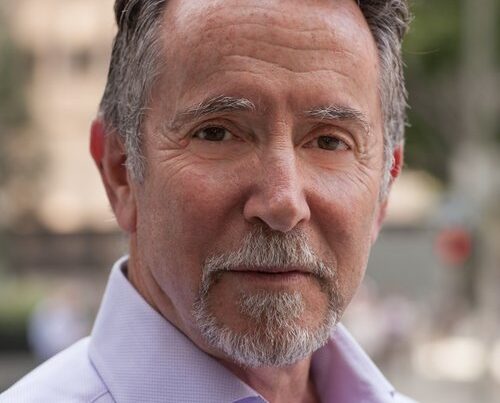

Allen C. Buchanan, SIOR, is a principal with Lee & Associates Commercial Real Estate Services in Orange. He can be reached at [email protected] or 714.564.7104. His website is allencbuchanan.blogspot.com.