Lessee accounting: What has changed?

As mentioned above, the legacy guidance shows that a clear distinction exists with how lessees record operating and capital leases. Operating leases are off-balance sheet items and capital leases get recorded as a liability and capital asset at present value.

Under the new standards, the classification of leases has changed, along with their placement on the balance sheet. Other changes and common challenges addressed include:

- The definition of a lease

- How initial direct costs are defined

- More extensive disclosure requirements

- The treatment of lease and non-lease components

Lease accounting under the old standards, ASC 840 and IAS 17

| FASB | IASB | |

| Standard | ASC 840 | IAS 17 |

| Lease Types | Capital lease and operating lease | Finance lease and operating lease |

| Classification of Lease | Determined based on criteria of 4-part test (ASC-840-10-25-1) | No specific criteria, but the substance of the transaction |

| PV of Min. Lease Payment | Lesser of the incremental borrowing rate or known implicit rate (ASC-840-10-25-31) | Incremental borrowing rate or known implicit rate |

| Location |

Capital – on balance sheet Operating – off balance sheet |

Capital – on balance sheet Operating – off balance sheet |

Lease accounting under the new standards and major differences

| FASB | IASB | |

| Standard | ASC 842 | IFRS 16 |

| Lease Types | Finance lease and operating lease | Finance lease |

| Classification of Lease | Determined based on the criteria of a 5-part test | All in-scope leases are classified as finance leases |

| Location | Both finance & operating leases will be listed on the balance sheet (except short-term operating leases) | All leases will be listed on the balance sheet (except short-term operating leases and certain low value leases) |

| Reporting | New quantitative and qualitative disclosures | Qualitative disclosures are required |

Who is affected by the new standards?

All companies that lease assets are affected by the new standards. Some considerations exist within both ASC 842 and IFRS 16 to omit specific types of transactions from capitalization (i.e. short-term leases). However, all companies that have the right to use at least one in-scope asset that qualifies as a lease will need to apply the new standard.

Industries that are most affected by the lease accounting changes

The changes under ASC 842 and IFRS 16 will have wide-ranging effects across most industries.

| Industry | Potential Compliance Challenges |

| Healthcare |

|

| Manufacturing |

|

| Logistics & Transportation |

|

| Energy, Oil & Gas |

|

| Retail & Restaurants |

|

| Banking & Financial |

|

Why embedded leases are a particular challenge

One of the biggest challenges companies face today involves identifying their embedded leases. A typical real estate lease can require legwork to gather the appropriate data, but the process of identifying the lease itself does not provide immense difficulty.

Embedded leases, which refer to leased assets provided within service, outsourcing, and maintenance contracts, require additional work. Examples of contracts that may contain embedded leases include:

- Warehousing contracts – although typically outsourced, these agreements may contain language that meets the definition of a lease.

- Security contracts – these types of services may also contain access to scanners or equipment, which could qualify as a lease under the standard’s definition.

- Transportation contracts – depending on the terms, the vehicles used for transport could qualify as a lease asset

- Data storage contracts – much like security contracts, these agreements could include embedded leases for both the servers or the space the servers occupy.

Departments responsible for procurement will not typically have a comprehensive understanding to know whether the contract includes any assets that qualify as an embedded lease. The process of dissecting each contract for embedded lease assets might just earn the title of the most daunting exercise that the lease accounting transition requires.

Common lease accounting errors under ASC 840 that could impact your transition

Beyond what’s required when adopting the new accounting standards, there are many additional errors that are common within current lease accounting. One of the initial steps in ensuring compliance with the new standards is, of course, to ensure that no current errors exist within lease accounting today. Any such errors in your current accounting will present additional challenges when your organization is transitioning.

For example, there exists a practical expedient under ASC 842 that allows for the grandfathering of lease classification. Sounds great, right? Keep in mind that this practical expedient can only be applied if there are no errors associated with the classifications of your current leases. Are you sure that you applied the capital lease criteria correctly for each one of your leases?

Below, we’ve noted six common errors in lease accounting and provided links to some additional articles that will help you find and apply the right solution.

1. Incorrect lessee accounting for tenant improvement allowances

When a lessee receives a tenant improvement allowance (TIA), they often do one of two things, both of which are incorrect: they either do nothing or they reduce the value of the leasehold improvement by the amount of the allowance. This is common in situations where the landlord pays a contractor directly for the improvements rather than paying the tenant.

Neither of these methods are correct under ASC 840, however, and they will cause accounting problems. They could understate the value of a leasehold improvement as well as the associated depreciation expense, impacting EBITDA.

To learn the correct guidance for tenant improvement allowances under ASC 840, read our blog, “Tenant Improvement Allowance Accounting the Correct Way.”

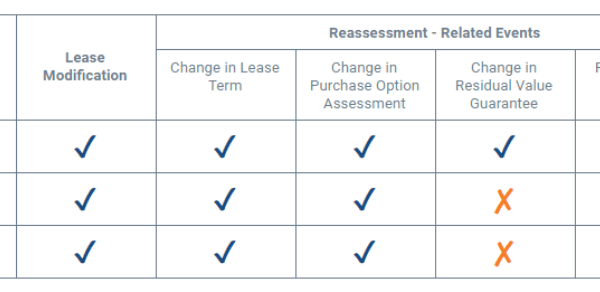

2. Accounting for tenant improvement allowances when a lease is renewed or modified

Another common error associated with TIA accounting is related to leases that are renewed or modified. Often, lessees will simply do nothing at all to compensate for these changes. However, this is incorrect. When a lease is renewed or modified prior to the end of the initial lease term, the lessee should reassess the straight-line reduction in the incentive liability account based on the new lease terms.

When companies do not make any changes to the TIA amortization schedules after a lease is renewed or modified, then rent expense is understated in some years and overstated in others. This can also impact EBITDA.

The previously-referenced article on TIAs contains a full example on the correct guidance for this issue. Additionally, to learn more about lease modifications, read the following articles: