When your business is in a financial bind, proactively negotiating rent concessions is a smart strategy for getting relief while you seek additional funding or ride out an economic downturn. Rent deferrals offer businesses an opportunity to temporarily reduce overhead while still complying with the financial obligations of their rental agreement. While landlords miss out on income in the short-term, they may be willing to take on the risk for tenants who make a strong case that the relationship will be beneficial in the long run.

In the event of a larger financial crisis, whether it be a global recession or industry-wide slump (such as the “Retail Apocalypse” of the last decade), landlords may be overwhelmed by requests for rent concessions. The likelihood of reaching favorable terms rests on your ability to stand out as a good candidate for deferment. Use these tips to make your case.

1. See the landlord’s perspective

When you approach a landlord seeking a rent deferral, they have to find other ways to fulfill their mortgage, tax, utility, and other financial obligations that come with owning the property without the income they earn from your rental agreement. Since this money is likely coming from their financial reserves, they need to know that you will be able to meet the terms of the agreement so they can replenish their savings. Your financial statements, revenue trends, and past history as a tenant will all come into play.

The landlord needs to feel secure that your business will remain solvent through the terms of the deferment. At the same time, they want to make sure that your business actually needs financial relief, and isn’t attempting to temporarily boost the bottom line. Be prepared to demonstrate that the financial challenges you’re facing are real, but also temporary, and that you can continue to be a good tenant in the long run.

2. Know the full value of your lease

Another factor your landlord will be considering is the overall value your lease holds in terms of the larger property and/or their entire portfolio. What’s the impact of potentially losing your business as a tenant? Does your business draw in foot traffic, name recognition, or employees who patronize other businesses on the property? An anchor retail shop in a mixed-use development will have greater success than a fledgling coffee shop in the same space. Being able to communicate your lease’s value to the landlord’s overall portfolio can provide leverage in your negotiations.

3. Use data to identify which leases to negotiate

When the new lease guidance was released in 2016, the objective was to provide investors and stakeholders added visibility into the full-scope of businesses’ financial obligations. But an added benefit is that it also provides companies with greater insight into their lease portfolio. Companies that have started or completed their transition to the new lease standard are at an advantage in being able to identify which leases are best candidates for negotiation.

When leases are fully inventoried and stored in a lease accounting system, stakeholders from throughout the company can create reports that encompass the entire portfolio, or filter by entity, asset class, or any segmentation of their choosing. Granular reporting and forecasting features make it easier to make focused decisions about your lease obligations. Companies that are still managing lease data in silos will have a much harder time making this determination. This is another reason why, despite the delays to the compliance deadline for some companies, companies should continue to make progress towards adopting the new standard.

4. Approach with a solution in mind

By approaching your landlord with a solution – instead of an open-ended request to negotiate, you give an indication of your willingness and ability to follow through on the terms of the request. In addition to the length of the deferral and payback periods, consider these provisions in your request to negotiate:

- Are you requesting to defer base rent or the additional rent as well?

- Can some of your deposit be used towards rent?

- Are you willing to pay interest on the deferred payments?

- Are you willing to offer up additional collateral to give the landlord extra security?

Keep in mind that these kinds of agreements can have accounting implications. You want to make sure that your accounting department is engaged in the process so they can proactively address any impact to your books and financial records.

5. Collaborate across departments

Rent deferrals have an impact on multiple departments throughout your business, particularly if you pursue them for multiple leases. It’s important that representatives from finance, accounting, treasury, and real estate/operations are in communication with each other to help determine whether deferment is an ideal option, and if so, which leases to defer and for how long. Each team has access to tools (such as software) that can be valuable in the planning process, and may have insights that can help in negotiations.

While your accounting department may not drive the rent deferral negotiation process, they will have to brace for how that negotiation impacts the preparation of financial statements. Keeping them in the loop makes that process more efficient and reduces the likelihood of accounting errors at the end of the year.

6. Understand the accounting implications of rent deferments

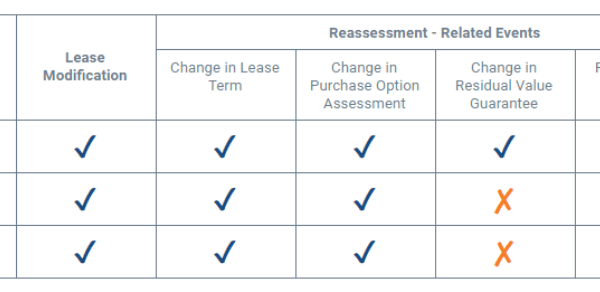

It’s important to consider how the terms of your deferral will be reflected in your financial statements, particularly as you transition to the new standard, which calls for a more complex treatment of lease modifications. Under ASC 840 and ASC 842, rent concessions may qualify as lease modifications. The modification guidance under both standards is complex and may be time consuming for both lessees and lessors.

COVID-19 relief guidance

Because of the financial and resource strain caused by COVID-19, the FASB issued relief guidance that provides companies some reprieve from the arduous task of identifying and accounting for rent concessions as lease modifications. The FASB Staff Q&A on this topic outlines that if a rent concession was granted as a direct result of the COVID-19 pandemic, companies may elect to treat it as if it was part of the original contract. What this means is simplified accounting for both the lessee and lessor as they can elect to account for these types of rent concessions outside of the modification framework in ASC 842 and ASC 840.

There are a few caveats to electing this policy:

- The lease concession must be a direct result of the COVID-19 crisis.

- There must be a documented agreement between the lessor and lessee to defer rent payments.

- The policy election must be applied to all concessions on contracts with similar characteristics.

- The concession must result in revised consideration for the lease that is substantially the same as, or less than, the consideration for the lease immediately preceding the change.

If the terms of the deferment agreement require you to extend the contract by a substantial period of time, such as 24 months, this represents a significant increase in the lease term and contract consideration. That would not qualify for application of the FASB’s relief guidance for COVID-19 related rent concessions. For more information, take a look at our step-by-step walkthrough of how to account for deferrals under the FASB’s relief guidance.

When deciding whether to elect the optional relief guidance, accounting departments need to be aware of the full terms of the deferment. Making policy elections and communicating them to auditors and other stakeholders early in the process can prevent stumbling blocks down the road.

Strong negotiation starts with good communication

Ultimately, your landlord will be more likely to agree to defer rent if you are a proactive, clear communicator. While the relationship between the landlord and your business sets the foundation for a good negotiation process, the strength of your data, financial statements, and overall understanding of your lease’s role in the landlord’s portfolio can help you drive it home.

Related articles

For more information regarding modifications, please review the following articles.